By Richard Mawarire (Economist)

What is now widely known as the Big Bang traces back to the 27th of October 1986 when the then Finance Minister of Britain Nigel Lawson within a day passed laws which saw the London Stock Exchange (LSE) being privatised.

Prior to this move the London Stock Exchange was a paltry 1/13th in terms of volumes of trade when compared to the New York Stock Exchange (NYSE).

The deregulation which came with the Big Bang is to this day credited for transforming London into the Financial Capital that it is today, competing with New York, Beijing, Frankfurt among others.

The sort of courage that informed Nigel Lawson is probably what Zimbabwe needs to untangle itself from the dilemma confronting it on the currency question.

This article seeks to trace how the currency crisis developed over time from 2014 to 2018 using key monetary statistics and how the situation evolved over time. Informed by the reality that the economy is slowly redollarising, this discussion will close with a solution on how to implement a Big Bang Inspired solution together with the key success factors that will anchor such a radical decision.

Evolution of the Currency Crisis

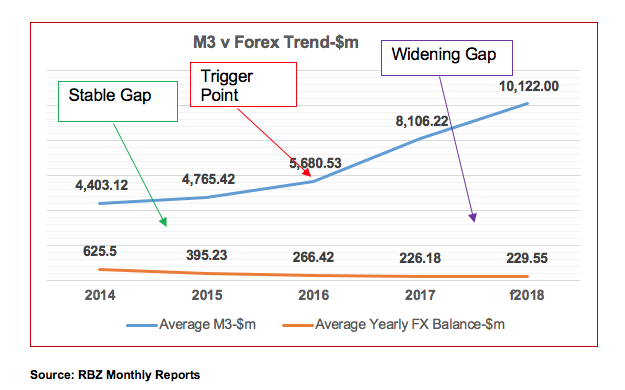

From 2014 to 2018 the economy has registered a sustained growth in money supply underpinned by an expansionary fiscal framework during that period. This saw the money supply grow by 130% from $4.4b in 2014 to $10.1b in 2018.

This growth however was not matched by a corresponding increase in the stock of foreign currency (USD Cash Notes, Coins and Nostro). The stock of foreign currency fell from $625m in 2014 to $225m in 2018.

As shown in the diagram below the ratio of Foreign Currency expressed as a total of broad money supply(M3) fell from a high of 15% ($0.15c per every $1) in 2014 to 3% ($0.03c per $1) in 2018. This accounts for the biting USD Cash notes and Nostro crisis that characterised the market from 2016 to date.

Over the years the economy has suffered a massive mismatch between money supply and the supply of foreign currency. There are at least three observable periods (as shown in the diagram below) in the evolution of the foreign currency crisis.

Over the years the economy has suffered a massive mismatch between money supply and the supply of foreign currency. There are at least three observable periods (as shown in the diagram below) in the evolution of the foreign currency crisis.

Between 2014 and 2015, the supply of foreign currency was relatively stable and the gap between Money Supply and Foreign currency was not as pronounced (Stable Gap). However, there was a trigger point in 2016 when the gap between Money supply and foreign currency began to worsen.

This is the same year that saw the introduction of bond notes and huge government expenditures on Agric related subsidies as the government embarked on the Special Maize Import Substitution Programmes (Command Agriculture).

The third phase of the currency crisis depicts a widening gap between Money supply and foreign currency holdings. Without a significant increase in foreign currency holdings, money supply grew from $5.6b in 2016 to $10.1b in 2018.

This growth was matched with a decrease in the supply of foreign currency from $266.4m in 2016 to $229.55m in 2018. This period saw the emergency of the alternative market with premiums rising to over 245% for USD and RTGS.

Solution X- The Big Bang Approach

Solution X- The Big Bang Approach

With a dose of Nigel Lawson’s courage, the monetary authorities need to make a quick and radical decision to address the currency dilemma. First and foremost there is need to restore the Foreign currency to Money supply ratio to 2014 levels when it was around 15% ($0.15c per $1). This can be achieved through two options: the rebasing of the broad money supply and a simultaneous foreign currency injection:

- RTGS/Bond Notes rebasing

The principal objective with this option will be to reduce the Broad money supply(M3) figure from $10.1m currently to 2014 levels ($4.4b). This means there is need to eliminate $5.7b off the circulation. In typical Big Bang Approach this can be achieved by fixing the RTGS/USD rate to $1.76: $1 and converting all RTGS and Bond Notes to USD and allowing businesses to trade in USD at 1:1 afterwards. This approach should be coupled with the following:

- $400m Foreign Currency Injection

As the RTGS and Bond Notes balances are rebased, there is need for a minimum cash injection of c$400m into the economy so as to show up the ration of foreign currency to money supply. However, the $400m has to be earmarked towards productive sectors of the economy and should not be our typical consumptive expenditure.

Critical success factors for the Bing Bang Approach

Critical success factors for the Bing Bang Approach

It will be a serious oversight for the authorities to assume that the Big Bang Approach will work miracles without the necessary enablers. The following will need to be put in place for such an approach to work:

- Banking sector consultations

Since banks are central to the financial system, there will be need for extensive consultations to agree to a perfect framework on how to implement the Big Bang Approach. This has to be done to ensure there is minimum disruption to financial sector stability. A special dispensation might need to be sought on the treatment of long-term loans or advances made to the government via instruments like Treasury Bills among other considerations.

- Stakeholder Engagement

There will be need for a comprehensive stakeholder engagement process covering business, civic society, citizens and other economic agents for the monetary authorities to explain the rational of such a move. This helps in getting the necessary buy-in upon which trust and confidence can be built.

- Transparent Forex Allocation process.

In the letter and spirit of the proposed New Foreign Currency Allocation Committee by the Finance Minister, there will be need to make transparent all transactions relating to the weekly allocations of foreign currency in the economy. This will give the transacting public the much needed confidence in the financial system and reduce leakages.

- International community goodwill

The need for the international financial institutions to extent their goodwill can never be overemphasised if this solution is to work. Zimbabwe on its part would need to demonstrate a clear commitment to austerity and adhere to a clear arrears clearance strategy and a commitment to real austerity as pronounced in the Transitional Stabilisation Programme(TSP).

There will also be need to work towards the clearance of outstanding issues harbouring the repeal of ZIDERA and other restrictive measures.

In conclusion this article sought to put across the option that the authorities have if they are to implement a Big Bang Approach to solving the currency crisis. Minus the short-term pain that this approach might inflict, the Big Bang Approach appears the only feasible option as the economy already shows signs of slowly redollarising.

Let the good times roll!

Richard Mawarire is Head of the Economic Research Cluster of the Young People’s Dialogue (YPD). Feedback on [email protected] or Whats App +263772242941

Discover more from Nehanda Radio

Subscribe to get the latest posts sent to your email.